Only one in four Americans thinks their credit score is an accurate reflection of their financial status, new research suggests.

That’s according to a recent survey with a panel of 2,000 respondents, 80% of whom (1612) identified as current homeowners.

Of those polled, just 28% strongly agree that their credit score accurately represents their financial situation.

About one in nine respondents (12%) feel their credit score is lower than it should be, and another 50% actually feel their credit score is higher than it should be, including slightly more homeowners (51%) than non-homeowners (46%).

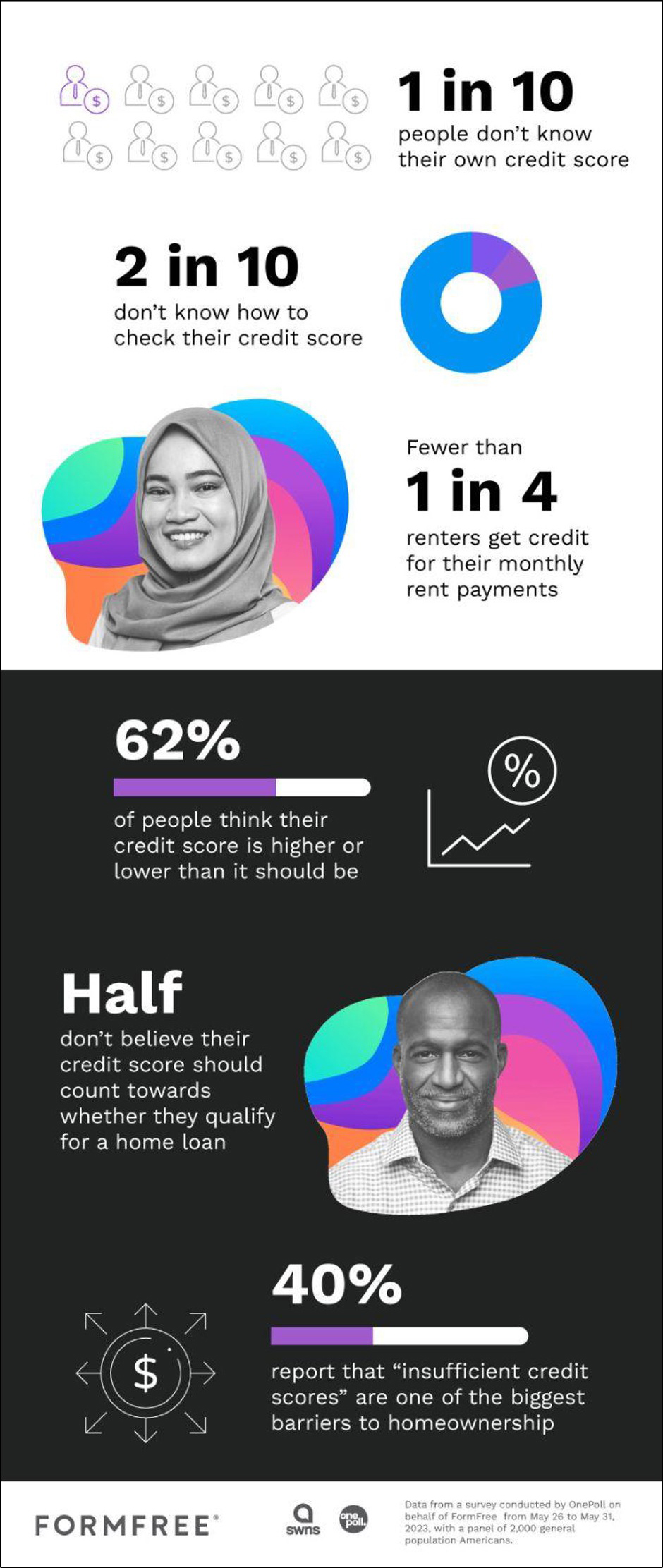

Moreover, one in ten Americans have no idea what their credit score is, and one in five wouldn’t know how to check it.

Conducted by OnePoll on behalf of FormFree, the survey also revealed that only half of Americans believe their credit score should count towards whether or not they qualify for a home loan.

While 49% said that their credit score should be considered, another 53% would prefer that their ability to pay their bills on time should also be factored in.

With all that in mind, it’s not surprising that only 50% of non-homeowners are confident that they’ll one day be able to afford a house.

Respondents believed that a credit score between 670 and 769 would be needed to secure a mortgage – leaving out the 20% who put their current score at somewhere under 669.

When prompted to describe their general perception of credit scores, four out of five (81%) chose not to categorize them as “necessary.”

Forty percent even cited “insufficient credit scores” as one of the biggest barriers to homeownership for the average American, just under “difficulty qualifying for a mortgage loan” (42%) and “insufficient savings for a down payment” (43%).

“It is astonishingly rare for credit bureaus to receive comprehensive reports on consumers’ payment history from landlords or utility companies. At a time when the average monthly rent is higher than the average mortgage payment in many U.S. cities, only 24% of renters are getting credit for managing their housing expenses,” said FormFree CEO Brent Chandler. “This lack of data fails to provide a fair assessment of individuals’ financial management skills and undermines the accuracy of credit evaluations when used without deeper cash-flow analytics.”

Overall, the average respondent makes between three and four (3.78) financial transactions in a day on essentials like gas, laundry or groceries.

Two-thirds (69%) of respondents admitted that they don’t feel they can leave the house without spending money in some way, new research suggests.

“Mortgage lenders have a tremendous opportunity to improve their assessment of loan applicants’ ability to pay by considering consumers’ overall cash flow instead of solely relying on traditional credit scoring models,” Chandler added. “Only 28% of consumers view these models as transparent, while a significant 40% express a preference for a more open home financing process where lenders compete to offer the best terms. It’s time to embrace a more holistic approach that benefits both consumers and lenders alike.”

Top 5 Biggest Barriers to Homeownership

- High housing prices in the market (49%)

- Insufficient savings for a down payment (43%)

- Difficulty qualifying for a mortgage loan (42%)

- Insufficient credit score (39%)

- Limited job stability or income (34%)

Survey methodology:

This random double-opt-in survey of 2,000 general population Americans was commissioned by FormFree between May 26 and May 31, 2023. It was conducted by market research company OnePoll, whose team members are members of the Market Research Society and have corporate membership to the American Association for Public Opinion Research (AAPOR) and the European Society for Opinion and Marketing Research (ESOMAR).